Bad Credit Mortgage Rates

Written and verified by Sophie Waugh - Last Updated 23/01/2023

Learn all about bad credit mortgage rates here. We go through how bad credit affects the deals and lenders available to you, what your options are & more.

Excellent

4.88 Average rating

Speak to a Mortgage Advisor

Fill out this form and we'll contact you to book a free call with one of our mortgage experts.

Typically, someone with bad credit won’t have access to as large a pool of lenders and products as someone with great credit. This means you may be limited to higher interest rates and have to meet stricter criteria.

While this is the overall rule, it isn’t always the case. The main things to know about getting a mortgage with bad credit is that the lenders and deals available to you will depend on the nature of the bad credit, how recent it was and your overall situation.

In this guide we’ll go through everything you need to know about bad credit mortgage rates.

The Topics Covered in this Article Are Listed Below:

- What Is Bad Credit?

- What Is the Lowest Credit Score Required for a Mortgage?

- How Does a Mortgage with Bad Credit Work?

- Can I Get a Bad Credit Mortgage?

- What Deposit Do I Need for a Mortgage with Bad Credit?

- How Can I Increase My Chances of Getting a Mortgage with Bad Credit?

- Will Applying for a Mortgage Harm My Credit Score?

- Summary: Best Bad Credit Mortgage Rates

What Is Bad Credit?

When we talk about bad credit concerning mortgages, it generally refers to personal financial issues marked on your credit report. They can vary from missing one phone payment to bankruptcy and can impact your credit score to varying degrees. The following situations are considered forms of bad credit:

- Having little credit history

- Late or missed payments

- Default payments

- CCJs (county court judgements)

- IVAs (individual voluntary arrangement)

- Debt management plans (DMP)

- Mortgage arrears

- Repossession

- Bankruptcy

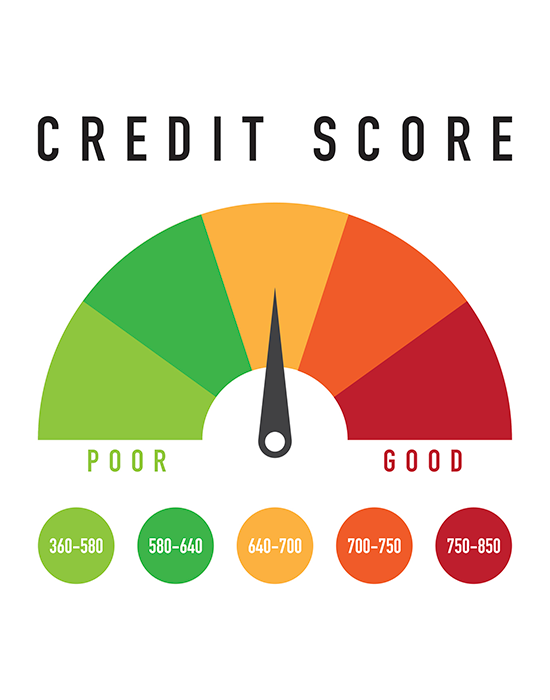

What Is the Lowest Credit Score Required for A Mortgage?

There’s no minimum credit score required for a mortgage, but the lower your credit score, the smaller the pool of lenders that will consider your application and the lower your chances of securing a great deal.

Let’s explain how it works. Bad credit events such as missed payments can negatively impact your credit score which is indicative of your overall credit profile. Most lenders assign you a credit score when considering your application. They use the information held by credit reference agencies – e.g. Equifax, Experian and TransUnion – to do this.

Some lenders, such as those specialising in bad credit mortgages, don’t credit score in the traditional way. They look at each application on a case-by-case basis and learn about the circumstances that led to the bad credit event.

This means that while a high street lender may reject you because of a bad credit event, a bad credit mortgage lender will be more likely to consider you. A specialist mortgage broker like John Charcol can help you find a lender to suit your circumstances.

How Does a Mortgage with Bad Credit Work?

Lenders who accept mortgage applications from people with low credit scores tend to call these "bad credit mortgages". These work in the same way as normal mortgages, but they may come with higher interest rates, fees and/or deposit requirements depending on the lender.

Bad credit mortgage lenders tend to charge higher rates and have stricter criteria due to the perceived additional risk of lending to a borrower with a history of poor credit or bad credit events.

If you're approved for a bad credit mortgage and keep up with your repayments, you should see your credit score improve over the following 2 or 3 years. You may then have the option to remortgage onto a better rate.

Can I Get a Bad Credit Mortgage?

It's possible to get a mortgage if you have a low credit score or bad credit history. But you'll likely find it more challenging than someone with a clear credit history. A bad credit history will reduce the number of lenders prepared to approve your application for a mortgage. The good news is that many lenders specialise in bad credit mortgages and our advisers at John Charcol can help you identify the right one for your situation.

Lenders take into account several significant risk factors when assessing mortgage applications. This means that you must ensure that everything else in your circumstances matches the lender criteria, for instance, the type of property you want to buy and its affordability. It will also greatly help your position if you can put down a larger mortgage deposit than the minimum.

As soft searches are usually carried out during the DIP (decision in principle) stage of the application process, you can get a good idea of whether you're likely to be accepted without damaging your credit file with hard searches. If you're concerned about the type of searches the lender will use at the DIP stage, check with the broker or lender beforehand.

What Deposit Do I Need for A Mortgage with Bad Credit?

Generally, the higher the deposit you can put down, the better the interest rates you'll be offered – this also applies with bad credit mortgages. With a lower LTV (loan-to-value), you'll pose a lower lending risk, meaning you could be offered a better rate.

LTVs are usually a maximum of 95% for a residential mortgage and 75% - 85% maximum for a buy-to-let mortgage. It's common for the maximum LTV to be lower for bad credit mortgages.

How Can I Increase My Chances of Getting a Mortgage with Bad Credit?

While having bad credit can make getting a mortgage more complicated, you can maximise your chances of being accepted by:

Using a Specialist Mortgage Broker

As an independent, specialist mortgage broker we have access to lenders and deals from across the whole market. We’re also experts in bad credit mortgages which means we can match you with the right lender with the best deal for your situation.

What’s more, most bad credit lenders only operate via an intermediary like John Charcol. This means that you’ll have a much easier time securing a good deal with the help of a mortgage broker.

Saving Up a Larger Deposit

The larger the deposit you can put down, the better the interest rate you may be able to access.

Checking Your Credit Report

Out of date information and errors on your credit report can damage your credit score, so it's a good idea to check that all the details on your file are correct. There are 3 main credit reference agencies in the UK that you can check: Experian, Equifax and TransUnion. If you spot any mistakes, contact the credit agency and ask of an amendment.

Building Up Your Credit Score

Credit scores can be impacted by all sorts of bad credit events - from missed credit card payments to bankruptcy. Luckily, it's possible to rebuild your score over time and show potential lenders that you can be responsible with money. Learn how to improve you credit score.

Getting Your Finances in Order

Sorting out your finances helps you take control of your money and can greatly improve the likelihood of being approved for a mortgage. A few useful things you can do include:

- Put any spare money you have into savings for a deposit

- Reduce as many outstanding debts as possible

- Pay all your debt payments and bills on time

Will Applying for a Mortgage Harm My Credit Score?

Every mortgage application you make shows up in your credit report as the lender performs a hard credit check. This means that if your mortgage application is declined, it could negatively impact your score. Being declined by several lenders will inevitably have a significant effect. So it's good idea to speak with a mortgage broker who can ensure you only apply with lenders that soft credit check at the DIP stage and who have criteria you’re able to meet.

Being accepted for a mortgage can cause your credit score to drop temporarily as you've taken on more debt, but as long as you meet your payments on time it will ultimately improve your credit score.

Summary: Best Bad Credit Mortgage Rates

Securing a mortgage at a competitive rate when you have a bad credit history can be extremely challenging, especially if you try to go at it alone. Working with a specialist mortgage broker like John Charcol can increase your chances of getting a bad credit mortgage and securing a cheaper rate.

We’re a whole of market broker and we’re bad credit mortgage experts. We learn about your situation and use our knowledge to approach the right lenders with the best deals, making your experience as straightforward and easy as possible.

Get in touch with us today on 0330 433 2927 to find out how we can help you.

First-Time Buyer Mortgages

Discover the best first time buyer mortgage rates available and the latest advice from John Charcol: mortgage broker for first time buyers.

Applying for a Mortgage

Applying for a mortgage couldn’t be simpler with our easy and simple guide from application to accepting your offer.

How Much Can I Borrow?

This mortgage calculator examines your income and works out how much money a mortgage lender might provide you with

House Buying Mortgage Guide

Are you looking to buy your first home? Or perhaps want to move to a new area? Our step-by-step guide will tell you everything you need to know about buying a house.

Help to Buy Guide

Support from the government-backed Help to Buy initiative is available for first-time buyers and existing homeowners who are finding it difficult to move up the housing ladder.

House Mortgage Deposit

Saving a mortgage deposit for a house is definitely one of the biggest hurdles you face as a buyer. In our guide we explain how deposits work and ways you can save.

Mortgage Deposit Amounts

Learn all about the different mortgage deposit amount options, how they affect your mortgage, how they vary depending on what type of borrower you are & more.

Funding Home Improvements

There are a few ways to finance work on a house: get a home improvement loan, remortgage for home improvements, ask your lender for a further advance & more

Mortgage Glossary

On this page you’ll find our detailed mortgage terminology glossary. There’s a lot of jargon out there but we’re here to make it easy.